The 2026 AI Chip Shift: Why Tech Giants Are Finally Moving Away From NVIDIA

For the past three years, the tech world has operated under a single, undeniable hegemony: the NVIDIA era. From the H100 to the Blackwell B200, Jensen Huang’s silicon has been the “digital gold” fueling the generative AI explosion. However, as we pass the midpoint of 2026, the landscape is shifting. The “NVIDIA Tax”—characterized by eye-watering margins and punishing lead times—has finally pushed the world’s most powerful companies to a breaking point.

We are currently witnessing the “Great Diversification.” Tech giants are no longer content being NVIDIA’s best customers; they are becoming its most formidable competitors. Here is why the monopoly is fracturing and what the new custom-silicon era looks like.

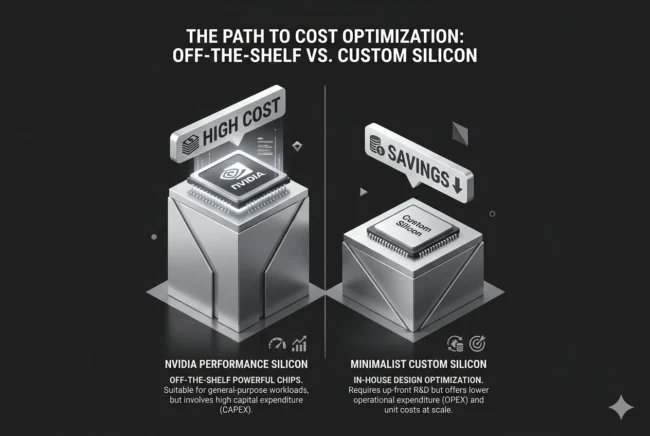

The Economic Imperative: Escaping the $40,000 Bottleneck

The primary driver behind the shift is, unsurprisingly, the bottom line. NVIDIA’s enterprise GPUs are among the most expensive components in the history of computing.

The Margin Gap: While NVIDIA enjoys gross margins upwards of 75-80% on its high-end AI chips, hyperscalers like Microsoft and Meta are seeing their capital expenditure (CapEx) skyrocket.

Total Cost of Ownership (TCO): Buying an H200 is just the beginning. The power consumption, cooling requirements, and proprietary networking (InfiniBand) lock companies into a high-cost ecosystem.

Supply Chain Sovereignty: In 2024 and 2025, waiting for an NVIDIA shipment was the biggest bottleneck in tech. By designing their own chips, companies like Google and Amazon can control their own production timelines with foundries like TSMC.

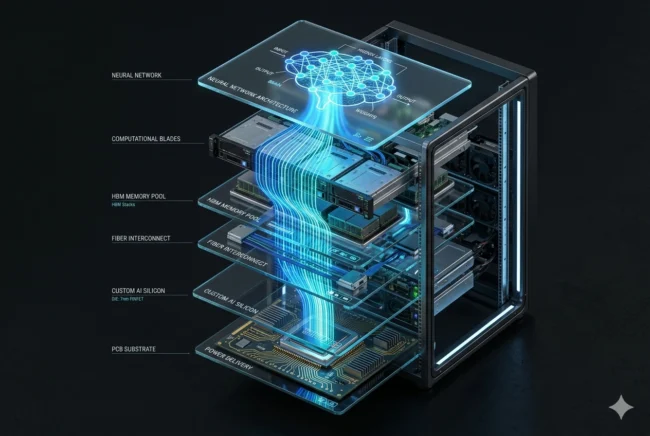

Vertical Integration: The “Apple Silicon” Playbook

The most successful tech strategy of the last decade has been vertical integration. Just as Apple transformed the Mac with M-series silicon, the “Magnificent Seven” are doing the same for the datacenter.

Software-Hardware Synergy: When you control the LLM (like Gemini or Llama 3) and the silicon it runs on, you can strip away “general purpose” GPU fluff. Custom ASICs (Application-Specific Integrated Circuits) are designed to do one thing—tensor math—with surgical precision.

Instruction Set Optimization: Tech giants are increasingly leaning into RISC-V and custom ARM architectures to bypass the overhead of legacy GPU instructions that aren’t necessary for transformer-based models.

Memory Efficiency: By integrating HBM3e (High Bandwidth Memory) directly into their custom architectures, companies are achieving 2x the memory-to-core throughput of a standard PCIe-connected GPU.

The Inference vs. Training Divergence

In 2023, the world was obsessed with training massive models. In 2026, the focus has shifted to inference—the actual running of these models for billions of users. NVIDIA’s architecture, while brilliant for training, is often seen as “overkill” and inefficient for pure inference tasks.

The Power Wall: Running inference on a Blackwell GPU is like using a Ferrari to deliver groceries. It’s fast, but the gas mileage is terrible.

Low-Precision Specialization: New custom chips from Meta and Amazon are optimized for FP8 and even FP4 precision, allowing models to run with a fraction of the electricity required by a high-end NVIDIA part.

Latency at Scale: For real-time applications like AI voice assistants and vision-processing, custom silicon allows for “Single-Batch” inference, reducing latency to near-instant levels that general-purpose GPUs struggle to match.

The 2026 Leaderboard: Who is Building What?

The “AI Chip Mess” of 2027 we discussed in the Snapdragon roadmap is reflected here in the datacenter. Every giant now has a “secret” silicon lab.

Google (TPU v6 & v7): Google is the veteran here. Their Tensor Processing Units are now in their 6th and 7th generations, powering nearly 100% of the Gemini infrastructure. They have effectively “opted out” of the NVIDIA race for internal workloads.

Amazon (Trainium 2 & Inferentia 3): AWS is aggressively moving its cloud customers toward its own chips by offering 40% better price-performance than NVIDIA-based instances.

Meta (MTIA v3): Mark Zuckerberg’s “Meta Training and Inference Accelerator” is now live across their datacenters, handling the massive recommendation algorithms for Instagram and Threads.

Microsoft (Maia 100 & Cobalt 100): Microsoft is finally reducing its multi-billion dollar dependence on NVIDIA to power Azure and OpenAI’s ChatGPT.

OpenAI (Project Tigris): Rumors persist that Sam Altman is securing hundreds of billions in funding to build a global network of AI foundries, aiming to produce an OpenAI-exclusive chip by 2028.

The “NVIDIA Moat” and the CUDA Barrier

Despite this massive shift, NVIDIA isn’t going anywhere. Their “Moat” isn’t just hardware; it’s CUDA—the software layer that nearly every AI developer on earth uses.

The Software Lock-in: Moving away from NVIDIA means rewriting massive amounts of code. While tools like Triton (OpenAI) and PyTorch are making it easier to port code to other chips, NVIDIA’s software ecosystem remains 5 years ahead of the competition.

The Software Lock-in: Moving away from NVIDIA means rewriting massive amounts of code. While tools like Triton (OpenAI) and PyTorch are making it easier to port code to other chips, NVIDIA’s software ecosystem remains 5 years ahead of the competition.

Sovereign AI: While Big Tech is building its own chips, entire nations (Saudi Arabia, UAE, France) are buying NVIDIA chips by the tens of thousands to build “Sovereign AI” clouds.

The Verdict: A Multipolar AI World

The “2026 Shift” marks the end of the AI Monarchy and the beginning of the AI Republic. NVIDIA will remain the luxury leader—the “Porsche” of the datacenter—but the heavy lifting of the global AI economy will soon be done by “Invisible Silicon.”

For users, this is a win. Increased competition leads to lower subscription costs for AI services and more efficient localized hardware. The era of the “General Purpose AI GPU” is fading; the era of the Workload-Specific AI ASIC has arrived.

Tech ReviewerFounder & Publisher: Sole operator and lead technical architect of MultiCore Performance

Areas of Expertise:

Silicon & Hardware Benchmarking: Firsthand performance testing and analysis of flagship processors specifically evaluating thermal and rendering capabilities in gaming and video editing workloads.,